A fun real estate story for Seth Macfarlane fans as the weekend approaches. Discover today’s mortgage rates and real estate trends.

See on www.youtube.com

A fun real estate story for Seth Macfarlane fans as the weekend approaches. Discover today’s mortgage rates and real estate trends.

See on www.youtube.com

Boost your Blog Content with these 3 helpful hints. Use content, graphics and video to drive more user interaction and improve your social network rankings. …

See on www.youtube.com

Real Estate TGIF May 23, 2014

The weekend is just around the corner. Learn about Mario Batali, #Seattle, and Home Buying. Discover how much buying power your have and where current mortgage rates are. #TGIF #RealEstate #MortgageRates

See on www.youtube.com

Current Mortgage Rates, 30 Year fixed rates, 15 Year fixed rates, 30 FHA fixed rates, 30 Jumbo rates, refinance, purchase loans. Throwback Thursdays, Sherloc…

See on Scoop.it – Real Estate and Mortgage Insights

FHA Back to Work – Extenuating Circumstances program allows borrowers to apply for a new mortgage loan only one year after losing a home. Previously, this waiting period was three years. In the program, borrowers may …

See on Scoop.it – Real Estate and Mortgage Insights

Mortgage rates were slightly higher today as a result of bond market weakness late yesterday and again this morning.

Mortgage Rates Watch

If your watching current mortgage rates to decide on locking or floating, originators and lenders are chiming in with their advice. #MortgageRates #Refinances #HomeBuying

See on www.mortgagenewsdaily.com

Taking out a mortgage can be exciting but stress-filled process. As if budgeting for a home and searching for an ideal property weren’t enough of a headache, the paperwork involved in the official mortgage application can prove to be time consuming and confusing as well. Before embarking on the application process, therefore, it can be helpful to know what information will be required of you, so you can compile all of the necessary documents and details ahead of time.

Taking out a mortgage can be exciting but stress-filled process. As if budgeting for a home and searching for an ideal property weren’t enough of a headache, the paperwork involved in the official mortgage application can prove to be time consuming and confusing as well. Before embarking on the application process, therefore, it can be helpful to know what information will be required of you, so you can compile all of the necessary documents and details ahead of time.

Personal Information

Of course, any loan application is going to ask you for your basic personal info (name, address, etc.), but mortgage loan applications ask you to detail your owning and renting history as well. Be prepared to enter information pertaining to your previous residences dating at least two years back, regardless of whether you rented or owned property. If you rented, the lender will contact your landlord to obtain information about your rent payments and any eviction histories. If you owned, the lender will require all information pertaining to previous mortgages and mortgage payment histories. If you are taking out the loan with a spouse or family member, keep in mind that both parties are required to provide this information.

Property and Loan Description

In addition to providing a detailed history of your previous residences, you will also need to describe the property you hope to purchase if granted the mortgage for which you are applying. The application will ask you not only to itemize the kind of loan you are requesting (i.e. whether it is a conventional loan or a government subsidized mortgage like an FHA loan), but will also ask you to describe the size and history of the property. You will need to list the year the property was built, the number of different rooms, the square footage, and any other necessary information. If you are taking out a construction loan, be prepared to list all of the anticipated construction and repair work planned.

Employment and Income Verification

Before filling out a mortgage application, you’ll also want to carefully compile information pertaining to your household income, including any assets or investments. Lenders will need to know how much you’re worth—and what kind of mortgage payment you can afford—before processing or approving a home loan. You will also be asked to provide the address and phone number of your current job, as well as a contact name so that the lender can verify your employment. If you have held your current job for two years or less, you will also be required to provide the same information with regard to your previous job.

When filling out a mortgage application, you will also be asked to itemize any liabilities—such as debt—that may impact your ability to make mortgage payments. It is important to be as accurate and honest as possible when providing this information, as accuracy will help you secure the most appropriate (and, in many cases, the lowest) mortgage rate possible.

In recent months, the housing market has seen steady improvement. Home prices and interest rates are up, but so are housing applications and purchases. While prospective homebuyers are demonstrating increased confidence in the market, this positive activity has also been somewhat tempered by the more stringent requirements set in place for lenders by the Consumer Financial Protection Bureau (CFPB) earlier this year.

In recent months, the housing market has seen steady improvement. Home prices and interest rates are up, but so are housing applications and purchases. While prospective homebuyers are demonstrating increased confidence in the market, this positive activity has also been somewhat tempered by the more stringent requirements set in place for lenders by the Consumer Financial Protection Bureau (CFPB) earlier this year.

New Stipulations

In early 2013, the CFPB approved a number of rules that restrict the activity of mortgage lending institutions. These rules prohibit lenders from granting loan terms that exceed 30 years, and they also forbid certain unique, special case conditions, such as periods in which homebuyers only pay interest on the principal loan. Additionally, mortgage fees are not to exceed 3% of the entire mortgage that’s granted, and the debt-to-income level of applicants must not exceed 43%.

Reasoning and Rationale

Some lenders are skeptical of these new regulations, seeing them as an infringement on their rights as independent institutions. However, as the CFPB stresses, the goal behind these new rules is to avoid another national economic crisis like the one triggered in 2008, when a glaring lack of regulation and oversight resulted in ultimately disastrous lending decisions. Relatedly, the new rules aim to decrease the risk involved for both buyers and lenders, as more stringent requirements increase the chances that a buyer will be able to successfully pay off the loan.

Immediate Effects

The individuals that will be most negatively impacted by these new regulations are those in the lowest socio-economic strata, who will likely be forced to rent rather than buy for a longer period of time. The age and income levels of first-time homebuyers will also likely increase, as lenders will require individuals to be more financially stable before granting them a mortgage loan. While this may be frustrating to some prospective buyers, it can also be beneficial, as it requires these individuals to be more financially savvy and conscientious about budgeting and saving to purchase a home.

Long Term Effects

In the long term, the members of the CFPB hope that the new regulations will help ensure that the economy continues to improve, as there will be fewer foreclosures and bankruptcy cases. These changes may also change the way we think about home ownership in America. As many economists have pointed out, America is one of the only countries in the world where owning a home is considered such a priority, and where even the poorest individuals in society are granted home loans. Over time, the number of families who choose to rent rather than buy may significantly increase.

If you are a prospective homebuyer who is about to undergo a mortgage application process, be prepared to face a slightly stricter evaluation and more extensive background check from your lender. While this may slow down the application process a bit, it is important to keep in mind that the lending criteria changes that are causing this delay have been put in place to protect you from future financial problems.

Recently, the 30-year fixed home mortgage (by far the most popular home loan available) has come under some scrutiny. Some argue that the loan should no longer be subsidized by private lenders, while others argue that it is the only way that most individuals would ever be able to eventually own a home. For now, though, the 30-year mortgage is here to stay, so here are some pros and cons of the loan that might help you decide if this is the right loan for you.

Recently, the 30-year fixed home mortgage (by far the most popular home loan available) has come under some scrutiny. Some argue that the loan should no longer be subsidized by private lenders, while others argue that it is the only way that most individuals would ever be able to eventually own a home. For now, though, the 30-year mortgage is here to stay, so here are some pros and cons of the loan that might help you decide if this is the right loan for you.

Pros: Affordability and Stability

One of the biggest draws of the 30-year mortgage is that in terms of monthly mortgage payments, it is often the most affordable. While many lenders recommend a 15-year mortgage, as the shorter loan term will reduce interest rates and help you pay off the loan more quickly, the increased monthly payments are simply not an option for many families. Moreover, the 30-year mortgage is offered at a fixed rate, meaning that your interest rates and payment amounts will not change over the life of the loan, unless you opt to refinance. This can be incredibly useful to those who need to do some long-term budgeting.

Pros: Initial Payments and Refinancing Options

The 30-year fixed rate mortgage also draws most homebuyers due to its low down payment requirements: often, buyers only need to put down 5% of the overall cost. These decreased down payment amounts generally apply even for those who qualify for hefty mortgages (loans can reach $3 million). Another benefit of the 30-year mortgage is that due to the long repayment period, it is fairly simple to arrange for refinancing when necessary. Thus, if interest rates improve over the life of the loan, you can refinance partway through to reduce your overall interest payments. The refinancing option can also be helpful if your house needs repairs, or if you need to consolidate debt under a lower interest rate.

Cons: Issues of Retirement and Major Expenses

For some, the 30-year mortgage option might be ideal. Yet this particular home loan might present some drawbacks to other homeowners, depending on their life stages, job situations, and family plans. For example, a 30-year mortgage would not be the best option for someone who is 15 years away from retirement. It might also present some difficulties to families who will be sending their children off to college at some point, since paying a mortgage on top of college tuition can be incredibly taxing on a family budget.

In an age when people move frequently for work and family-related matters, a 30-year mortgage can also be somewhat of a hassle. Of course, the biggest drawback of the 30-year mortgage is the amount of interest paid over a long term. In short, this mortgage is not the best way to save money on a home loan. To decide if this is the right home loan for you, take the time to plan out a long-term budget, and consider career, family, and retirement plans as well.

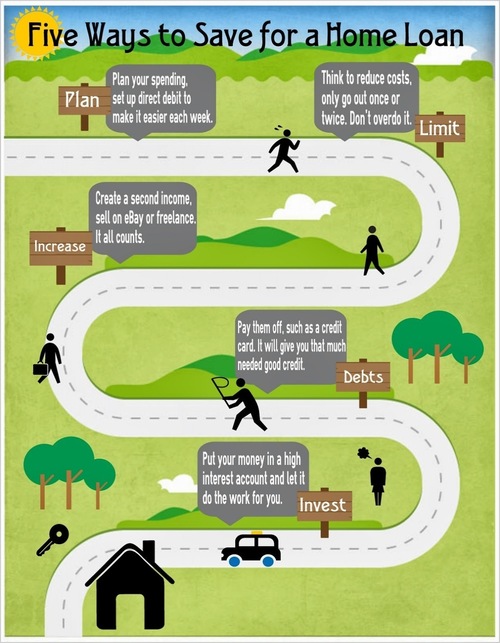

Since taking out a mortgage to purchase a home will likely be one of the most significant—if not the most significant—financial investment of your life, it’s important to plan for a mortgage application accordingly. This means making sure that all of your finances are in order and that your credit score is strong before going through the pre-approval process or signing on to any mortgage deal with a lender. What follows are some basic tips to help you with these preparations.

Since taking out a mortgage to purchase a home will likely be one of the most significant—if not the most significant—financial investment of your life, it’s important to plan for a mortgage application accordingly. This means making sure that all of your finances are in order and that your credit score is strong before going through the pre-approval process or signing on to any mortgage deal with a lender. What follows are some basic tips to help you with these preparations.

Pay Down Debt

One of the best ways to ensure that you get the best mortgage rate available is by improving your credit score, and one of the best ways to improve your credit score is by paying down credit card debt. By reducing your debt to income ratio, you can increase your credit score by as much as a hundred points, while simultaneously demonstrating to lenders that you are a responsible borrower and a sound investment for the bank. Paying off credit cards may sound like an intimidating task, and for those with a large amount of debt, it can take a while—all the more reason to start planning for a hone loan as far in advance as possible.

Avoid Additional Debt

Once you’ve paid down credit cards and credit lines, it’s also important to avoid accruing any new debt. This may seem like a no-brainer, but it can be very easy to slip back into new debt once old debt is paid off. Individuals feel a newfound sense of wealth and stability once credit cards are paid off, and occasionally use that as an excuse to take out an auto loan or open a store credit card account. This, however, can simply send your debt to income ratio skyward again, which in turn may threaten to lower your credit score and reduce your chances of getting the best loan rate out there.

Save, Save, Save

Of course, anyone who is looking to take out a mortgage should be sure they have enough money saved for a down payment. Yet it’s always a good idea to set aside more than you think you’ll need, as there will inevitably be some unexpected expenses incurred along the way to purchasing your home. For example, you may find your “dream home,” only to discover that the sellers are requesting a few thousand dollars more in a down payment, and will not budge in negotiations. Or you might find a house that seems right for you, but which will require a number of home repairs right away.

Finally, it’s important to keep apprised of the information on your official credit reports. Occasionally, these reports include erroneous information that may be driving down your credit score—and you don’t want to discover this problem when you’re sitting in the mortgage lender’s office. Make sure to request your official FICO scores prior to filling out a mortgage application, and be sure to comb through the documents to ensure that all of the information is correct.