At some point or another, many people face unexpected financial trouble that makes it difficult, if not impossible, for them to make their mortgage payments. In the face of these financial difficulties, whether they arise from job layoffs or other added expenses, some fear that foreclosure is their only option. This, however, is not the case—these days, loan modification is available as an alternative.

At some point or another, many people face unexpected financial trouble that makes it difficult, if not impossible, for them to make their mortgage payments. In the face of these financial difficulties, whether they arise from job layoffs or other added expenses, some fear that foreclosure is their only option. This, however, is not the case—these days, loan modification is available as an alternative.

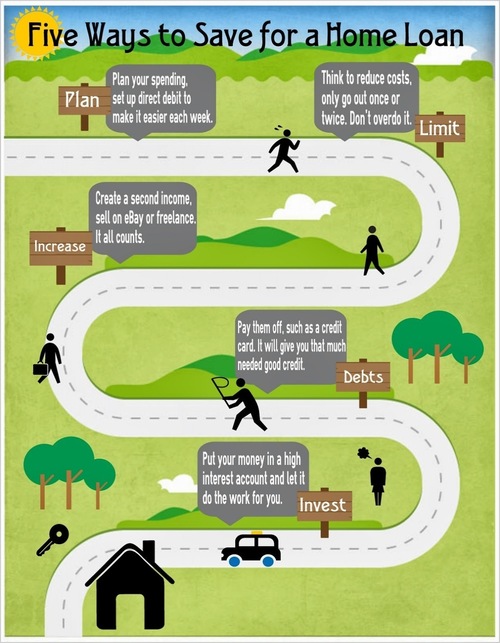

What is Loan Modification?

Loan modification is similar to mortgage refinancing in that the terms and conditions of the loan and/or loan payments are altered partway through the repayment. Whereas a refinance replaces an existing mortgage with a brand new one, however, loan modification simply adjusts the monthly principal and interest payments to accommodate drastic changes to a homeowner’s financial situation. Typically, loan modification periods are only temporary, intended to help homeowners just until they can recover from their financial issues. Some programs may last several months, while others can last a couple of years.

Government Loan Programs

In order to assist those families who are falling behind on their mortgage payments, and who thus may require a loan modification, the government has designed a program called The Home Affordable Modification Program (HAMP). This program was set up in response to the mortgage crisis of 2008, when thousands of individuals faced possible foreclosures. To help such struggling families keep their homes, HAMP sets forth guidelines to help mortgage lenders and borrowers as they navigate the ins and outs of loan modification.

HAMP Requirements for Borrowers

In order to qualify for HAMP assistance, homeowners must first be able to demonstrate clear evidence of financial struggle. To be eligible, the original mortgage must also have been approved no earlier than January 1, 2009. Homeowners must owe less than $730,000 on their mortgage (interest not included), and must also be able to prove that their current mortgage payment is at least 31% of their monthly gross income. Homeowners will also need to provide a significant amount of financial info, from income report documents to receipts from social security and disability payments, depending on the scenario.

HAMP Requirements for Lenders

As mentioned above, HAMP also sets forth guidelines for mortgage lenders, to ensure the smooth and efficient processing of any loan modification plans. For example, lenders are required to collect specific information from borrowers, including at least two of the most recent pay stubs from each person listed on the original mortgage, a detailed outline of the homeowner’s budget, the previous year’s tax returns, and a signed affidavit provided by HAMP. The servicer or lender in charge of the modification then submits all of the required documentation to HAMP coordinators.

If an applicant is approved for a loan modification, it is typically on a trial basis. For instance, most borrowers get the green light for a 3-month conditional modification; if they are able to successfully make the required payments during this time, then they can begin the official modification term. If they fail to make these payments, then foreclosure may unfortunately be the only alternative.